Two fundamental information sources, secondary and primary, are instrumental in conducting thorough technical and commercial analyses within the 3d Printing Sector. Our comprehensive study of the 3D printing sector leverages both, ensuring a balanced and robust understanding of this dynamic industry. Secondary sources, encompassing company websites, industry publications, news outlets, and specialized databases (such as OneSource, Factiva, and Bloomberg), provide a broad foundation. Complementing these are primary sources, derived from interviews with a spectrum of experts across core and related industries. These experts include key figures from suppliers, manufacturers, distributors, technology innovators, alliances, and standards and certification bodies within the 3D printing sector value chain. Their insights are crucial for understanding current dynamics, validating information, and forecasting future trends and opportunities in the 3D printing sector. Identification of key players in the 3D printing sector is initially achieved through secondary research, with subsequent primary and secondary research refining their market ranking. This rigorous approach includes analyzing company annual reports to pinpoint top performers and conducting interviews with key opinion leaders, including CEOs, directors, and marketing professionals, to gain deeper insights into the competitive landscape of the 3D printing sector.

Secondary Research in the 3D Printing Sector

Secondary research forms the bedrock of our investigation, employing a diverse range of sources to gather essential information about the 3D printing sector. This encompasses the examination of corporate filings like annual reports, investor presentations, and financial statements, alongside resources from trade, business, and professional associations. We also scrutinize white papers, specialized journals focused on 3D printing products, certified publications, and articles from recognized industry authors. Directories and comprehensive databases further enrich our secondary data pool. The objectives of this secondary research are to build a detailed understanding of the 3D printing sector supply chain, map its market value chain, identify the universe of key participants, and categorize the market based on industry trends down to granular segments. Geographic market analysis and the tracking of key developments, both from market and technology perspectives, are also crucial components. Data synthesized from these secondary sources allows us to establish initial market size estimations, which are subsequently validated and refined through primary research within the 3D printing sector.

Primary Research within the 3D Printing Sector

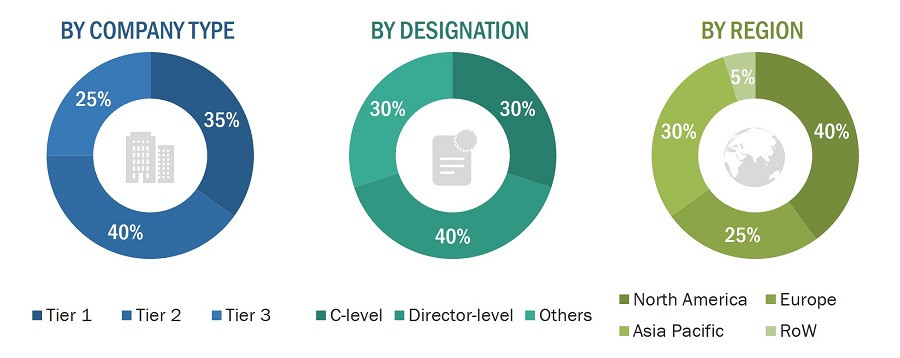

Building upon the foundational knowledge gained through secondary research, extensive primary research is conducted to deeply understand the nuances of the 3D printing sector. This involves numerous interviews with key opinion leaders from both the demand and supply sides of the market, spanning across four major global regions: North America, Europe, APAC, and the Rest of the World (RoW). Approximately 30% of these primary interviews target the demand side, while 70% focus on the supply side, providing a balanced perspective. The primary data collection is predominantly conducted via telephone interviews, accounting for 80% of the primary research interactions. Questionnaires and email correspondence are also utilized to gather data, ensuring a comprehensive capture of insights from key stakeholders within the 3D printing sector.

3D Printing Market Size, and Share

3D Printing Market Size, and Share

Alt: 3D Printing Sector Market Size and Share Analysis: Illustrative chart depicting market analysis for the 3D printing sector.

To delve into the underlying assumptions of this study and gain further details about our approach to analyzing the 3D printing sector, you can download the pdf brochure.

Market Size Estimation for the 3D Printing Sector

Our methodology for estimating and validating the market size of the 3D printing sector, along with its various submarkets, employs both top-down and bottom-up approaches. Key players operating within the 3D printing sector are identified through rigorous secondary research. Their market share within different regions is then determined through a combination of primary and secondary research methods.

This comprehensive research methodology incorporates the analysis of annual and financial reports from leading companies in the 3D printing sector, as well as direct interviews with industry experts. These experts, including CEOs, VPs, directors, and marketing executives, provide invaluable quantitative and qualitative insights. All percentage shares, market splits, and breakdowns are initially derived from secondary sources and subsequently verified through primary source validation. We meticulously consider all parameters that can influence the markets under study within the 3D printing sector. These parameters are thoroughly examined, validated through primary research, and analyzed to arrive at robust quantitative and qualitative data. This data is then consolidated and further enhanced with detailed analysis from MarketsandMarkets to inform our comprehensive report on the 3D printing sector. The impact of economic recessions is also factored into our market estimations for the 3D printing sector. The following sections detail the market size estimation processes employed in this study.

For the 3D Printing Sector market analysis, prominent manufacturers such as Stratasys (US), 3D Systems, Inc. (US), HP Development Company, L.P. (US), EOS GmbH (Germany), and General Electric (US) were identified as key players. Following confirmation of these companies through primary interviews with industry experts within the 3D printing sector, their total revenue was estimated using annual reports, SEC filings, and reputable paid databases. Revenues specifically attributed to business units offering printers, materials, software, and services within the 3D printing sector were then isolated from these sources. The aggregated revenues of key companies providing these offerings for the 3D printing sector were then calculated to estimate the overall market size. These revenue figures are further validated by industry experts through primary interviews, ensuring accuracy and reliability in our market sizing for the 3D printing sector.

3D Printing Sector: Bottom-Up Approach

3D Printing Market Size, and Bottom-Up Approach

3D Printing Market Size, and Bottom-Up Approach

Alt: 3D Printing Sector Market Size Estimation using Bottom-Up Approach: Chart illustrating the bottom-up methodology for market sizing in the 3D printing sector.

The bottom-up approach is instrumental in determining the overall market size of the 3D Printing sector by aggregating revenues from key players and considering their respective market shares. This method starts from granular data points at the company level and builds upwards to the total market estimation for the 3D printing sector.

3D Printing Sector: Top-Down Approach

3D Printing Market Size, and Top-Down Approach

3D Printing Market Size, and Top-Down Approach

Alt: 3D Printing Sector Market Size Estimation using Top-Down Approach: Diagram outlining the top-down methodology for market sizing within the 3D printing sector.

Conversely, the top-down approach begins with the overall market size to estimate the size of individual market segments within the 3D printing sector. This is achieved by applying percentage splits derived from both secondary and primary research. The most relevant parent market size is utilized as the starting point for calculating specific market segments using the top-down approach. Data gathered from interviews is consolidated, checked for consistency and accuracy, and integrated into our data model to determine market figures, aligning with the top-down methodology for analyzing the 3D printing sector. Market sizes across different geographic regions are identified and analyzed through comprehensive secondary research, further refining our understanding of the global 3D printing sector.

Data Triangulation in the 3D Printing Sector Analysis

After establishing the overall size of the 3D printing sector through the estimation processes detailed above, the market is further segmented into various segments and subsegments. Data triangulation and market breakdown procedures are applied, where appropriate, to complete the overall market engineering process and arrive at precise statistics for all segments and subsegments within the 3D printing sector. Data triangulation involves examining various factors and trends from both the demand and supply sides of the 3D printing sector. The market size validation for the 3D printing sector is rigorously conducted using both top-down and bottom-up approaches, ensuring a robust and reliable market assessment.

Market Definition of the 3D Printing Sector

The 3D printing sector is defined by the development of tangible, three-dimensional objects from digital models through additive manufacturing. This process involves constructing objects layer by layer using materials in solid, liquid, or powder form, typically in horizontal cross-sections. This additive approach distinguishes it from subtractive manufacturing methods. Also known as additive manufacturing (AM) or freeform fabrication, 3D printing in the 3D printing sector finds applications across tooling, prototyping, and the manufacturing of functional parts. These functional parts, produced via 3D printing, are utilized in a diverse array of industries including automotive, healthcare, aerospace, jewelry, consumer goods, art and architecture, and education, highlighting the broad impact of the 3D printing sector.

Key Stakeholders in the 3D Printing Sector

The 3D printing sector encompasses a wide range of stakeholders, including:

- Providers of 3D printing products and comprehensive solutions

- Service providers specializing in 3D printing related services

- Suppliers of 3D printing materials and accessories

- Consulting firms focused on the 3D printing sector

- Companies involved in 3D printing assembly

- Software providers for 3D printing applications

- Associations, organizations, forums, and alliances within the 3D printing sector

- Government and corporate entities with interests in 3D printing

- Venture capitalists, private equity firms, and start-up companies investing in the 3D printing sector

- Distributors and traders of 3D printing products

- End users seeking to deepen their understanding of 3D printing technologies and advancements within the 3D printing sector

Report Objectives for the 3D Printing Sector Analysis

This report aims to achieve several key objectives in relation to the 3D printing sector:

- To define, describe, and forecast the global 3D printing sector market size in terms of value, categorized by offering, process, technology, application, vertical, and geography.

- To project the market size, by value, for various segments within the 3D printing sector, focusing on four major regions: North America, Europe, Asia Pacific, and Rest of the World (RoW).

- To provide detailed insights into the primary factors driving market growth, as well as restraints, opportunities, and industry-specific challenges within the 3D printing sector.

- To deliver ecosystem analysis, case study analysis, patent analysis, technology analysis, ASP analysis, Porter’s Five Forces analysis, and regulatory context relevant to the 3D printing sector.

- To present a comprehensive overview of the value chain within the 3D Printing sector ecosystem.

- To strategically analyze micromarkets within the 3D printing sector, focusing on individual growth trends, prospects, and contributions to the overall market.

- To identify opportunities for market stakeholders by pinpointing high-growth segments within the 3D printing sector.

- To benchmark key players in the 3D printing sector using a proprietary Competitive Leadership Mapping framework, evaluating them across market rank and product offering parameters.

- To strategically profile major players in the 3D printing sector, comprehensively analyze their market shares and core competencies, and provide a detailed competitive landscape overview for market leaders.

- To analyze competitive developments within the 3D printing sector, such as partnerships, collaborations, agreements, joint ventures, mergers, acquisitions, expansions, product launches, and developments.

- To assess the impact of economic recessions on the 3D Printing sector.

Available Customizations for 3D Printing Sector Report

MarketsandMarkets offers tailored customizations to meet specific company needs regarding the 3D printing sector market data. The following customization options are available for this report:

Company Information

- In-depth analysis and profiling of additional market players (up to 7) within the 3D printing sector.